WeWork, or The We Company as it is now officially known, could launch its circa-$3bn US IPO as early as next week.

That’s despite some brutal commentary since the provider of flexible office space – or “space-as-a-service” if you subscribe to the spin – publicly filed with the SEC for its New York IPO on August 14.

It might even be said the press coverage WeWork and its co-founder Adam Neumann have received as the company prepares to go public is worse than Uber’s ahead of its debut in May. That’s saying something.

Here’s one cutting but hardly unique example of the critiques: WeWTF by Scott Galloway.

Galloway writes with impressive flourish and identifies plenty of red flags for investors contemplating this investment.

To rework the famous porcine analogy, WeWork is a pig caked in lipstick.

WeWork is “disrupting” real estate but instead of tenants, it has members. Instead of rents, it has membership fees.

Unfortunately, instead of profits (or funds from operations) you might associate with a REIT, WeWork has the big losses and poor corporate governance we have now come to expect from Silicon Valley unicorns.

After the disappointments of fellow “unicorns” Uber and Lyft earlier this year, investors are right to be very skeptical of this offering.

That said, the missing piece of information is what valuation WeWork is coming at. That won’t be known until the deal launches (next week or the week after).

The last private round led by Japan’s Softbank valued WeWork at $47bn but as Galloway points out, this investment came with a liquidation preference that means Softbank would get its money back first in the event of a sale or bankruptcy. In other words, it might not be a fair measure of WeWork’s value or any real indication of where underwriters will pitch the IPO.

WeWork has doubled revenues in the past two fiscal years and is on track to do it again this year. Though not necessarily a safe assumption, another doubling of revenues next year would see WeWork generating around $6bn of revenue (in calendar 2020). Put that on Uber Technologies’s current multiple of 4x-5x forward sales and you can get to a little more reasonable $24bn-$30bn valuation.

Reading the S-1 filing, there are clearly many other problems, including the company’s overly complicated corporate structure and related party transactions. These definitely should be discounted in the valuation.

Though it doesn’t really sound like Neumann’s style, a more reasonable valuation starting point would be one way to blunt the choral criticism.

Stocks are up for a seventh day and the pundits at CNBC and elsewhere think they will keep rising, but here’s a burning question.

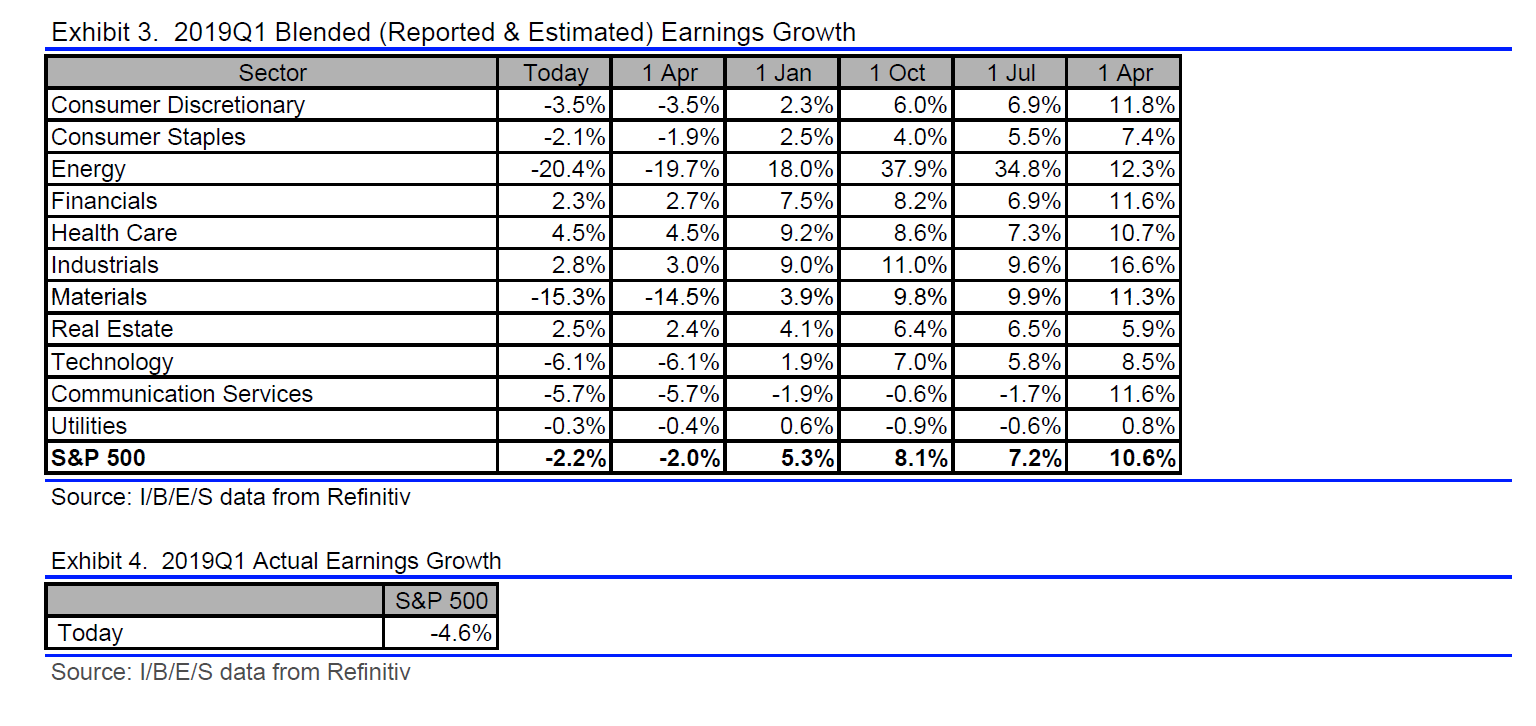

Why should stocks keep rising if their ultimate driver, earnings, are falling? That’s the expectation for Q1 and as the chart shows, earnings growth expectations have been dwindling consistently in past six months.

One reason is lower interest rates, though today’s good economic numbers don’t really support the case for a cut (whatever the President says).

If earnings ease and rate cuts don’t materialize, it will be hard for the run in stocks to continue. Or will it?

What is clear is that with the 2020 presidential election campaign warming up (easy to forget it is not until November next year), the current administration is eager to keep the economy and markets humming, whatever it takes.

The good news for investors is that after weak Q1 earnings growth, admittedly a function of outsized gains last year due to tax reform, growth should resume in the following quarters (see chart below).

Or at least that is what is in the forecasts, notwithstanding the likelihood they will be revised as time goes by.

Twitter is alight this morning with angst about newly public ride-sharing unicorn Lyft’s dismal second-day performance.

The stock’s slump below its $72.00 IPO price yesterday is at odds with reports that the offering was more than 20 times oversubscribed and Lyft’s nearly 10% gain on day one.

CNBC’s Jim Cramer, in particular, is taking some lumps for his rosy predictions, which just goes to prove that forecasting stock prices in the short-term is a mug’s business (remember that as you are watching CNBC). Still love ya Jim, despite what people say.

But how does a 20-times oversubscribed IPO trade below the offering price so soon after the deal?

This is far from the first time it (a high demand IPO that stumbles on debut) has happened, yet it remains a question whose answer eludes investors.

That’s partly because of the inherent lack of transparency of IPO demand and allocations.

But it can sort of be explained in broad terms.

Such disappointments tend to happen in situations like Lyft where the broader market is strong and the tech stocks are running (which is one reason a lot of IPOs are pricing now), but where there is no consensus on the company in question’s long-term prospects.

Lyft was able to justify a high IPO price/valuation (let’s say a high single-digit multiple of sales) akin to the hottest cloud software names, but it was by no means cheap.

“Not cheap” might be another way of saying that the company’s long-term prospects are not clear or that new investors (the existing ones not participating in the IPO are the true believers) are not sure whether they think this company will prosper long-term.

Offsetting this was the momentum behind the IPO in recent weeks (the hype) and the FOMO factor, the fear among investors they would miss out on easy gains by not participating in the IPO and look silly for doubting that momentum.

A couple of specific technical factors also contributed to the speedy reversal of fortunes.

The big one is that IPO allocations were very tight, so few institutional investors got enough stock to make Lyft a core holding. At the margin (which is all that is needed to determine stock momentum), many investors decided to sell when it became clear the early gains were going to be unsatisfying relative to the hype.

Additionally, Lyft debuted on the final day of the month/quarter, which may have given investors some incentive to book profits on the first day of the new quarter.

The other issue to keep in mind with all IPOs is the quality of the book of demand. If the shares go to short-term investors or hedge funds that see this as a momentum investment and don’t really believe in the business long-term, then it is hardly surprising they will sell when the momentum moves against the stock.

I think there are legitimate concerns about Lyft’s ability to make a profit long-term, which is central to the bear case. Cramer’s view is that Uber and Lyft are forming a duopoly that will eventually be able to lift prices. He could be right but he might not be.

The problem with this line of argument is that a large part of the value proposition for ride-sharing customers is price, and if the price is too high they will use public transport or their own cars.

The disruptive forces unleashed by unicorns have certainly been deflationary and may continue to be so for a long time as other competitors come up with twists on the ride-sharing idea and Uber and Lyft undercut each other to win the doubtful loyalty of drivers. Maybe you don’t really want to invest in an industry where price deflation is at play.

It is no surprise that Lyft and Uber are pursuing opportunities in autonomous vehicles since replacing human drivers would remove a big cost item (change the whole business model) and lead to lower prices for consumers (witness how so-called “monopolist” Amazon is looking to cut prices significantly at Whole Foods Market).

Offsetting this is that not all costs are going to be under the control of Uber and Lyft and governments will tax them (congestion pricing for instance) to help underpin the viability of public transport. That’s exactly what is happening in New York City at the moment.

All that said, Lyft still has an opportunity to prove the naysayers wrong and it is only day two. Theoretically the stock price doesn’t matter though it does if Lyft wants to come back to raise more capital, which it would have to do if it burns cash long-term.

Investors are not going to want to put more money into a losing investment and the company is not going to want to dilute existing shareholders by issuing stock at low prices.

It is possible that the stock continues to slump but more likely is that over the coming weeks it stabilizes somewhere in touching distance of the IPO price, giving the company a chance to wow investors with its first set of earnings (reported in early May).

This can work both ways. Facebook and Alibaba both saw their stock prices tumble in the early period after going public but have gone on to be fantastic investments. Then there are the disasters like Snap, Blue Apron and going back further, Groupon and Zynga, that saw lasting shareholder value destruction.

Investors really need to get straight in their minds whether Lyft (and soon Uber) is a Amazon/Facebook/Alibaba-type story or a Snap/Blue Apron.

There is some hope of the former because even if Lyft’s stock comes under pressure, the trends “driving” ride-sharing are likely to continue and Lyft might even become a target for big tech or maybe even an auto maker or a rental car company.

What does it mean for the Uber IPO next month? Well, Uber has waited so long to go public, it might be tempted to delay. Indeed the Lyft experience is more evidence the IPO market is broken.

But the impact on Uber may also be muted by investor recognition of its greater scale and wherewithal. All things being equal, it should win the long-term battle for ride-sharing marketshare simply because of the depth of its pockets.

Let’s see how Lyft trades today but the bears seem to be in charge for now (it was down again in early action today).

The IPO of ride-sharing unicorn Lyft is likely (this afternoon) to price at the top end of the upwardly revised US$70-$72 range or better after drawing huge demand from investors during the two-week roadshow.

Though there’s plenty of angst about Lyft’s cash burn and the fact it lost US$911.3m last year, at this point it simply doesn’t matter.

Reservations about the ride-sharing business model – in short, give it away if you have to, but get to scale as quickly as possible – and various regulatory issues are well-founded. But in Lyft’s case, these are questions for another day.

IPO investors want to invest in growth and companies that are doubling their top-line at scale don’t come along often.

Even if the overall market takes a breather here, companies that are growing at rates well in excess of the broader market and carving out new industries should fare relatively well.

This is probably why – somewhat counterintuitively – high-growth (tech) and defensive stocks outperformed in Q1, a quarter that saw the Federal Reserve become much more dovish and recession fears ease even with trade concerns top of mind.

Though Lyft’s financials are splotched with red ink, the growth is undeniable as is the potential size of the ride-sharing market if Lyft and Uber and others succeed in killing off household ownership of the automobile.

Anyway, that’s the potential. At this stage it is almost pointless to predict whether this happens and whether some other unicorn emerges with a even better model to deliver what Lyft calls “transportation-as-a-service”.

The IPO roadshow was standing room only and virtually everyone who got a chance put in an order.

Lyft made it clear in its filing it was not focused on short-term profits, or profitability at all, but investors won’t be too worried as long as the company is growing.

The lingering question is whether Lyft or arch-rival Uber, soon to follow with its own IPO, is the better bet.

I heard someone say yesterday that Lyft is just a smaller Uber with better PR. Of course, there are some differences between these companies in their geographical reach and the extent of their focus on other businesses, but it is true the ride-sharing experience is close to identical for customers.

Given the financial profile of the industry, that means the company with the deepest pockets is likely to have the most success.

Because of its larger size, Uber should be better placed to raise additional capital (equity, debt, convertible debt etcetera) and outlast Lyft in any extended price-based market share war in key cities.

That said, there may be room for both and investors at the moment clearly figure that Lyft is a great bet on the ride-sharing phenomenon.

Jeans maker Levi Strauss & Co surged 31.8% on debut today after pricing its IPO above range for base proceeds of $623.33m, the most confident sign yet a new-issue revival is under way after a disastrous start to the year.

Levi Strauss is the biggest IPO of the year so far and comes ahead of chunky near-term offerings such as Lyft, Tradeweb Markets and Change Healthcare, and maybe Uber (looking like April timeframe) as the biggest of them all.

The demand for Levi Strauss was clearly very strong, even stronger than you might expect for a company up against the vagaries of the fashion retail business.

This is a brand that has stood the test of time, the company has some growth (14% at the top line last year) and has been able to expand its margins by selling direct to the consumer, the trend that is likely killing off large parts of the traditional retail sector.

One reservation – apart from whether the company’s current growth is really sustainable – is that the controlling Haas family sold some of its stake at the IPO and may not be done. The prospectus is not explicit about their plans, which is probably intentional, but it means that a secondary sale is not out of the question later this year.

As investors counted their winnings, it was easy to miss that another IPO scheduled for this week, human resources software company Alight, opted to defer its IPO ahead of pricing tomorrow night.

Alight is backed by private equity firm Blackstone, which pulled the plug as investors showed reluctance to pay up inside the $22-$25 range for a company that is not growing as fast as the usual software IPO.

In fact, the way the financials are laid out in the prospectus, it is difficult to make prior-year comparisons.

The outcome shows that investors are not in a mood to buy anything, despite the dearth of IPOs so far this year. This could also be read as investors being extra cautious about current valuations, including those of the peers against which Alight was valued.

The other mark against Alight is its private equity backing, and it is a legitimate question whether the sponsor-backed IPO market, a major avenue for the monetization of sponsor investments, is broken.

Though Blackstone was able to bring a large number of its US portfolio companies public in the past five years, it hasn’t done so many in the past year or so.

The same goes for the other big private equity firms, now the center of much power on the Street (in part because they pay the biggest fees to investment banks).

The big miss last year was Apollo Global Management’s IPO of home security firm ADT. The deal priced well below range but ADT stock still trades at price less than half ($6.57 today) the level at which it went public at ($14) in January last year.

In fact, the private equity firms have produced some great public companies over a longer timeframe, but it is often the case that they perform poorly early on (2015’s First Data IPO is another classic example) because private equity firms on principle do not sell assets cheap.

Private equity firms have also gravitated to traditional industrial companies that can be bought cheap for their lack of growth but still generate consistent enough cashflow to support their financial engineering – that is, the pay down of hefty debt loads.

These companies typically come to market with high debt levels as a legacy of their leveraged history, though usually IPO proceeds are applied to bringing down debt to more manageable levels.

Change, a health IT company formed from a deal with drug distributor McKesson, is the next Blackstone portfolio company looking to get public. It is said to be looking to raise $1.5bn-plus but the Alight outcome suggests it is no fait accompli.

Uber or Lyft? Which to use is a question that has dogged New York’s ride-sharers for years.

With both poised to go public in the next month or two, the battle between these two bitter arch-rivals is about to extend to winning over the hearts and minds of the investment community. Things could get really interesting.

On Friday (March 1), Lyft started the clock for its IPO by filing publicly. It registered confidentially with the SEC on December 6, so it is already well advanced through the SEC review process. From all reports, the IPO roadshow will begin March 18 (it has to be at least 15 days after the public filing). With a standard roadshow, the deal should price on either March 27 or 28 before the stock debuts on Nasdaq the following day.

Cue plenty of (valid) commentary about the company’s cash burn and lack of profitability.

Multiply the media frenzy by four (?) once Uber files, which could well be in the next few weeks because (probably not coincidentally) it filed confidentially on the same day as Lyft.

Since it is more complex, larger and a more global beast, and the SEC is going to look really bad if it doesn’t work, Uber’s filing is said to be getting more scrutiny from the securities watchdog.

There is no doubt that ride-sharing is a social phenomenon that promises to revolutionalize and is disrupting transportation, and, depending on your perspective, for better or worse. Less clear is whether the numbers stack up.

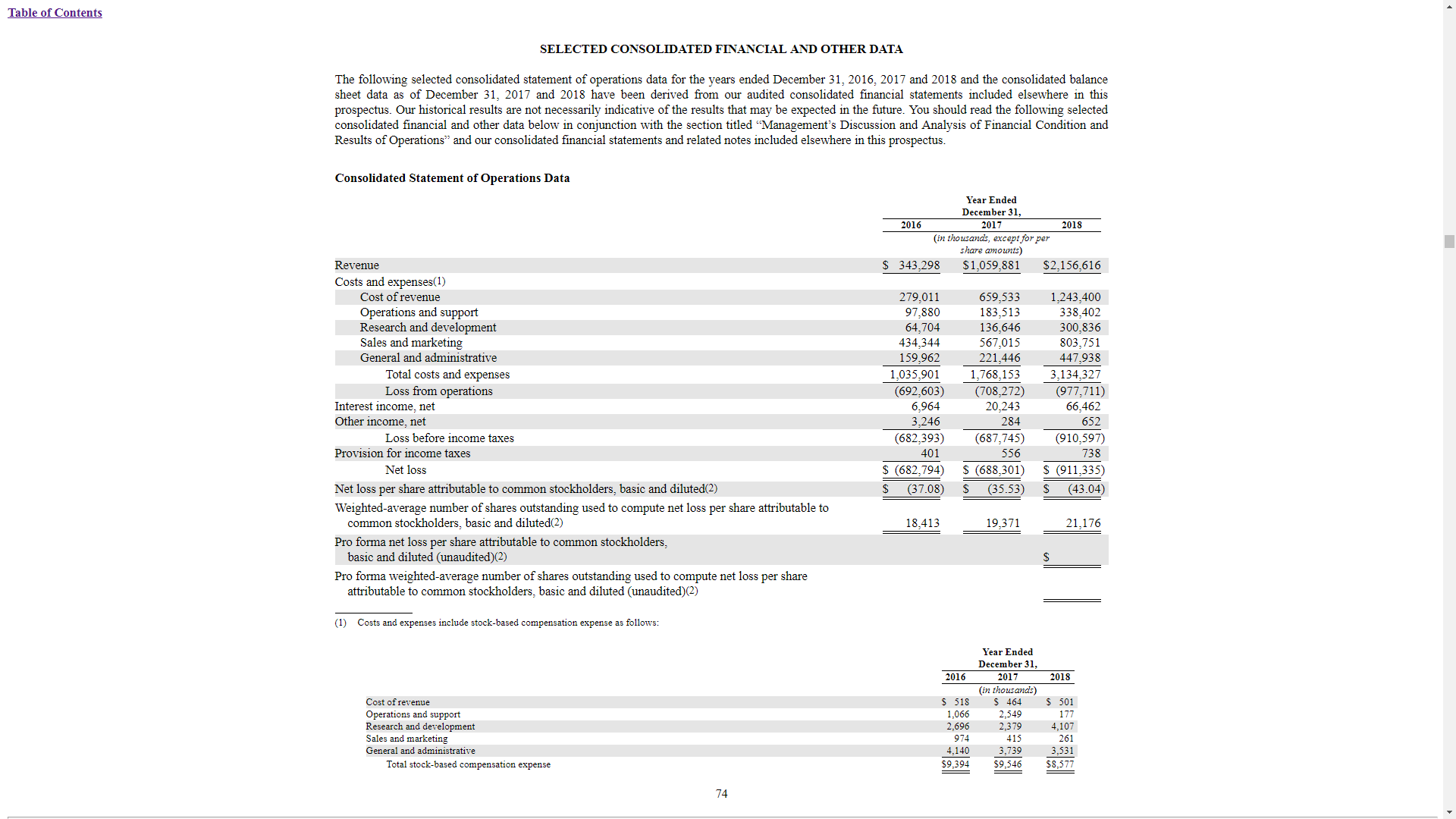

Lyft lost $911m last year (net loss but adjusted Ebitda is a similar amount) and burned through $281m of cash (based on its negative operating cashflows).

This is bracing stuff compared with the average IPO, but Lyft also doubled sales last year. Getting to even greater scale as quickly as possible, and outlasting other upstart competitors, is the priority.

I’ve seen IPOs that were growing that fast AND were very profitable at the time of IPO, but, counterintuitively, this can be a sign a company’s best days are behind it. The 2015 IPO of fitness band maker Fitbit is a good example. It presented some of the best financials ever seen for an IPO, but the deal came at or near the peak of its growth just as a host of competitors were able to come into the market with significantly cheaper products.

Though the IPO went well and the stock traded up initially, the deal didn’t stand the test of time. Fitbit stock now changes hands at just 30% of its IPO price.

More important for new investors is what Lyft’s financials will look like after this year and the coming years.

I thought the most interesting part about the filing (apart from the actual finances and the litany of legal actions the company faces) was the final part of the letter to investors from the co-founders Logan Green and John Zimmer.

“If we told you we were building the world’s best canal, railroad or highway infrastructure, you’d understand that this would take time. In that same light, the opportunity ahead requires continued long-term thinking, focus and execution. In order to best deliver long-term value, we will drive the business forward with three key principles:

“1.

We first serve drivers and riders.

“2.

We prioritize the long-term health of the business, over day-to-day reactions of the markets.

“3.

We thoughtfully balance investments in growth and profitability considerations, while deliberately leaning more towards growth (especially in these early days).”

Maybe it is just me but that doesn’t read like a company that is going to swing into profits anytime soon.

The question is: Does it matter? Much like Amazon, as long as the company continues to grow at above-market rates, it will be able to access capital and fund its growth without generating positive cashflow/Ebitda/profits etc.

That growth is the same reason why investors will swarm this IPO, the caveat being we don’t know the valuation.

At the mooted valuation of up to $25bn, Lyft would be coming at 12x 2018 sales or thereabouts (actually less using an EV/sales multiple that subtracts cash and equivalents from market cap used in the numerator)

The multiple comes down quickly if the company can continue something close to the current rate of growth, a doubling of its net revenues last year to $2.16bn.

It is a sure bet that market models will factor in high-growth for the next few years (50%-plus) at least.

Given there are not many growth stories like this around, this alone should ensure the IPO is heavily oversubscribed and (maybe) opens strong.

But whether these forecasts are right are a completely different thing.

Further out, things could be challenging, the fear being this could be more of a Blue Apron than Amazon-type situation. Blue Apron also had growth but huge cash burn in a new market (meal-kits) where the number of competitors offering introductory discounts multiplied quickly.

Lyft is actually the first-mover in ride-sharing but is dwarfed by Uber and there are quite a few other competitors too (Juno and Via in the US for starters).

So far ride-sharing is not like search (Alphabet/Google) and social media (Facebook) that have pretty much been winner-take-all markets, and not necessarily for the first-mover (Yahoo, MySpace).

But it could be, which is why Uber and Lyft are going public at the same time in a race to tap out equity capital providers first.

Talking to a number of NYC drivers in the past few days, it seemed they were all either using Uber exclusively or using both, but not Lyft exclusively.

According to one, using Lyft alone was not enough to make a living, which just highlights how Uber has the upper hand in markets like NYC and probably elsewhere too.

So even though Lyft has more room to grow by virtue of its smaller size, those that doubt the industry’s economics will sustain multiple players are going to back Uber instead.