A lot of people are talking about the outsized influence that Cathie Wood’s Ark Investment Management has on technology investing.

Though I am not one to buy into the hype (particularly for things like bitcoin), there’s something to be said about focusing solely on disruptive technology investments at a time when there is no lack of capital around to fund big ideas.

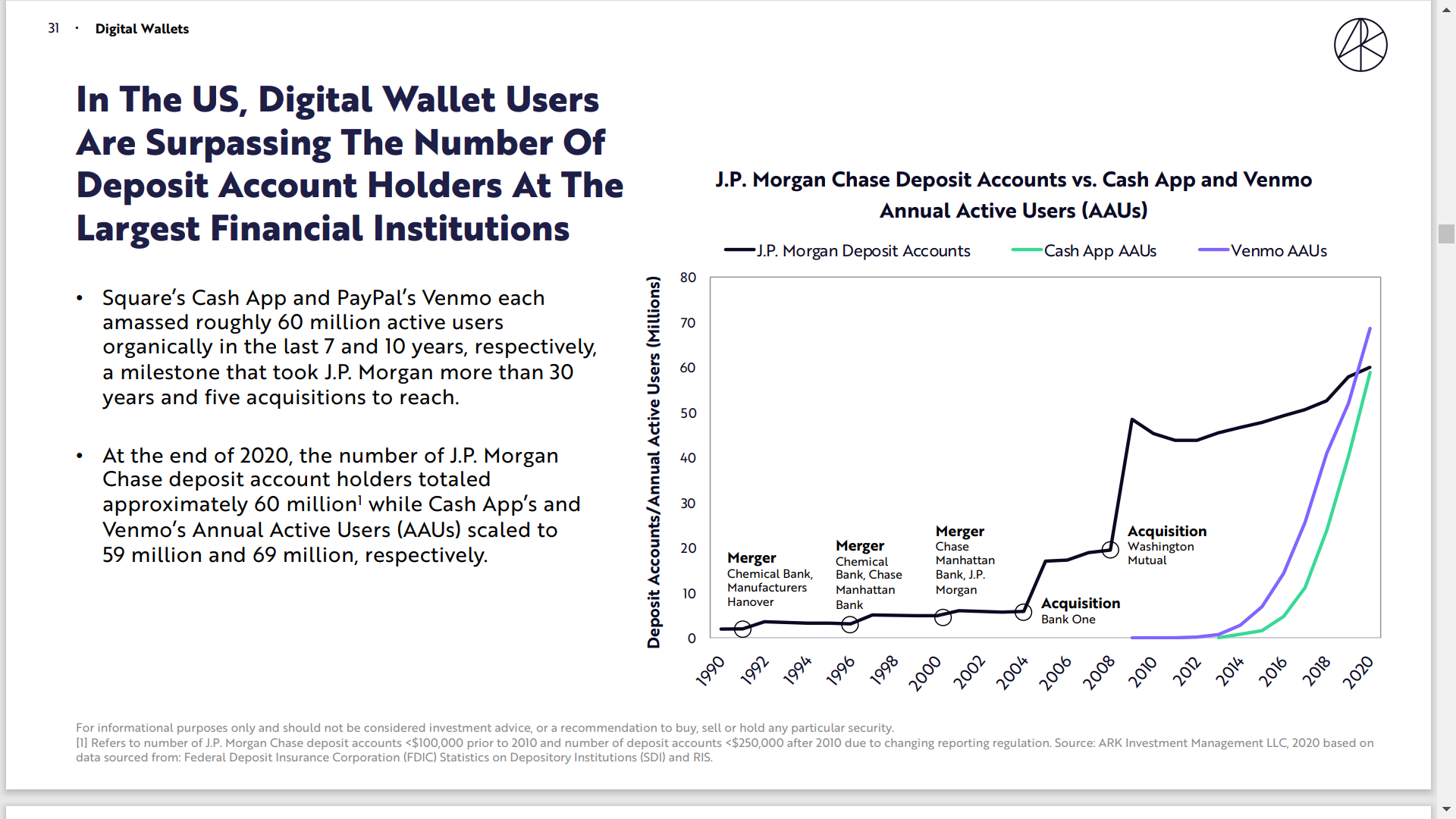

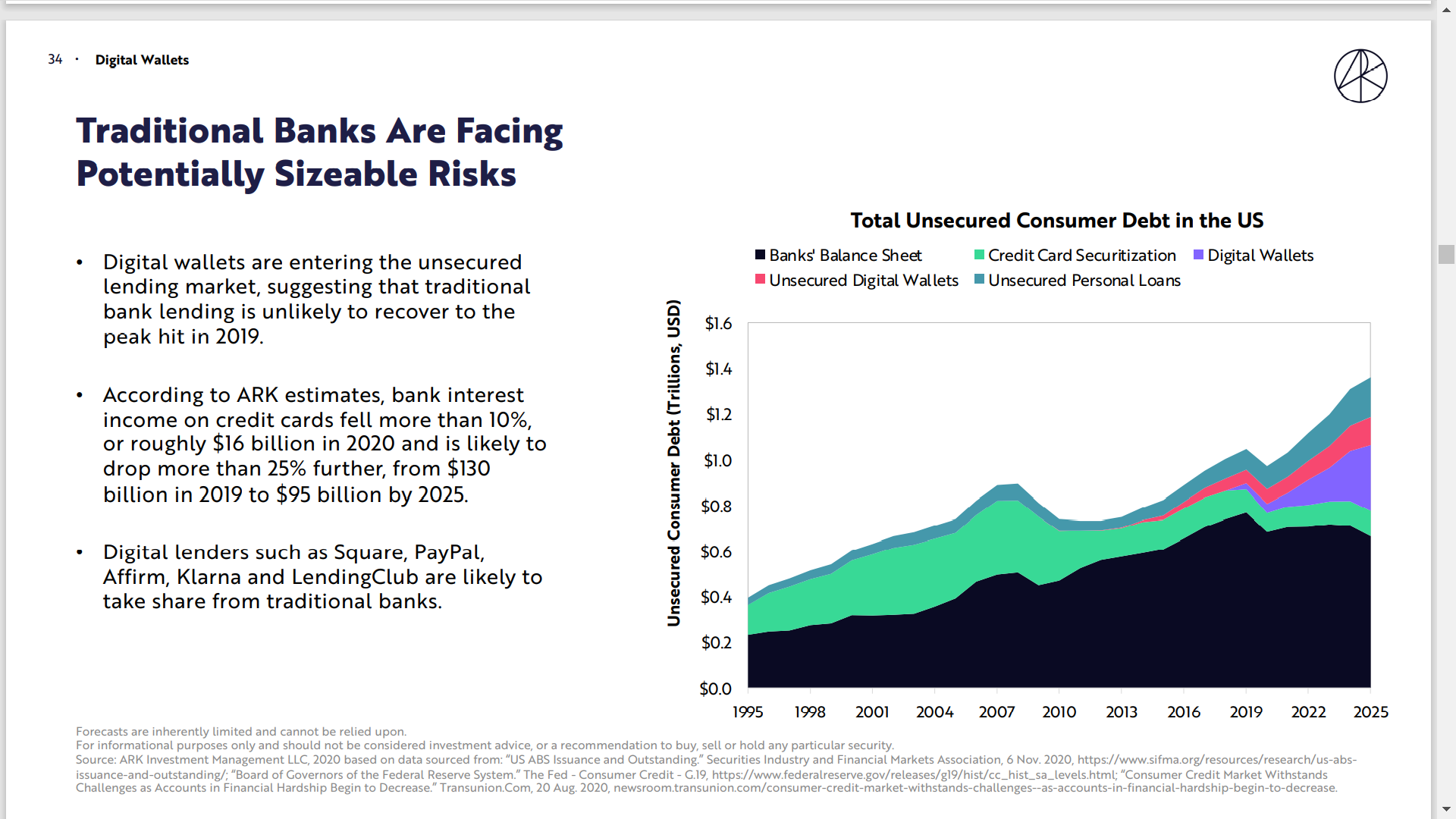

This recent report from Ark Invest on their “Big Ideas” is definitely worth a look. There’s a lot here, but to start with here’s some charts that caught my eye on the issue of fintechs eating the banks’ lunch.

Something is going to have to give re banks and their credit card businesses. It’s getting harder to justify charging such high rates in a low interest rate/easy money environment and they will need to do more to show consumers the value of rewards programs.

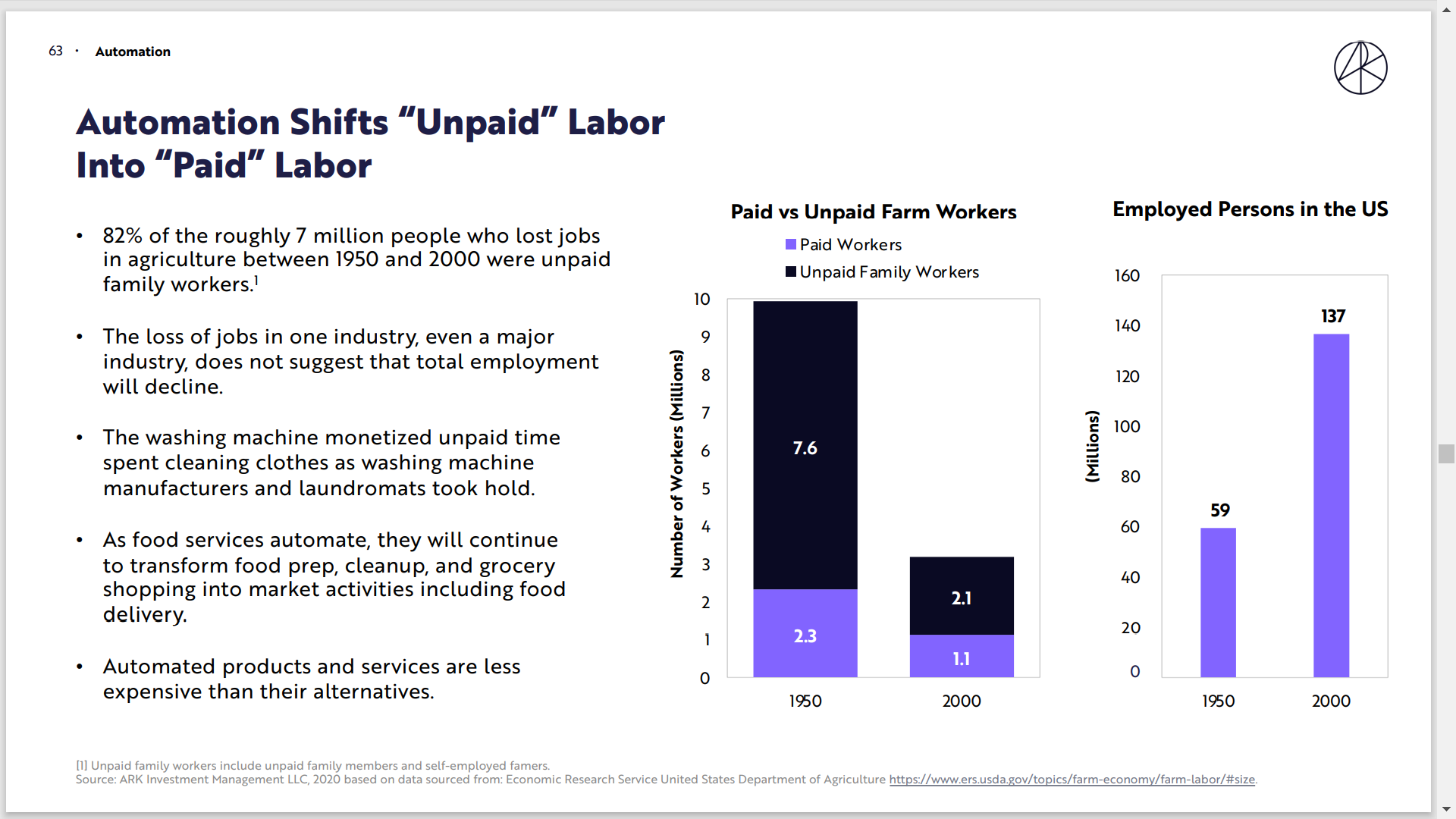

And one on automation and the counterintuitive impact on the labor market:

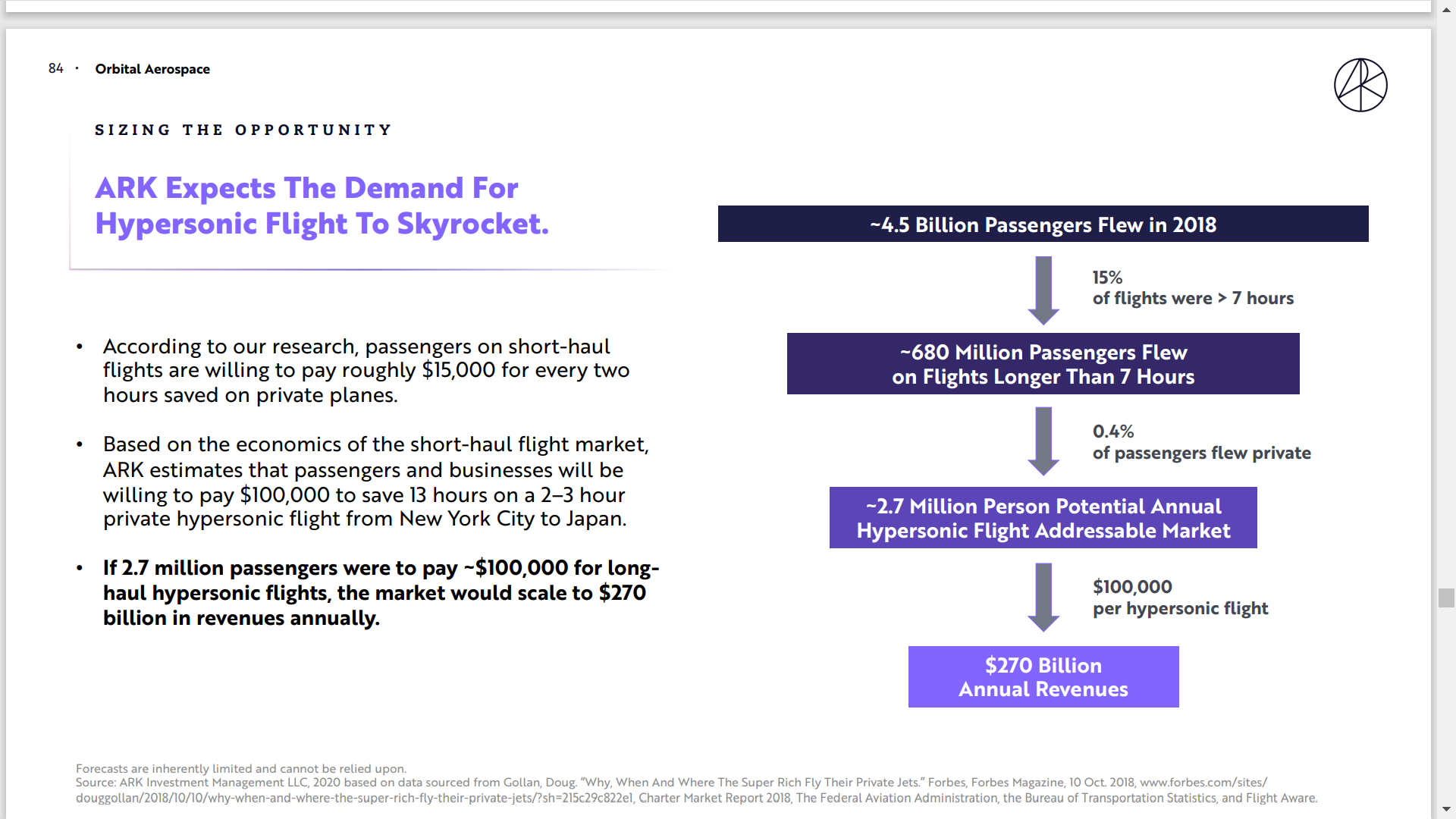

And hypersonic flight! (though I don’t think people will really be paying that much for a flight once it scales)…

It’s a VERY happy Valentine’s Day for Bumble CEO Whitney Wolfe Herd. On Thursday, Wolfe Herd (reportedly) became the youngest female CEO ever to take a US company public when the Austin-based dating app’s IPO raised $2.15bn and the shares surged about 63% on their Nasdaq debut.

By the end of the week, Bumble was carrying a market cap of $15bn (and she owns about 10% of the company herself). That’s mind-blowing considering private equity firm Blackstone took control of Bumble barely a year ago in a transaction that valued the company at just $3bn.

Now I don’t know, maybe there were some non-financial reasons why Blackstone found such a willing seller in Russian entrepreneur Andrey Andreev, who started Badoo in 2006 and then helped Wolfe Herd start Bumble in 2014. The umbrella Bumble company that went public owns both Bumble and Badoo, the former being the “women-first” mostly US-centric app and Badoo being better known internationally.

Consider here that Blackstone not only takes home the bulk of the IPO proceeds (around $1.7bn of the proceeds are being used to buy back its equity interests), but it still holds a roughly 60% economic interest in the company.

Blackstone also collected the bulk of a $330m debt-funded distribution to pre-IPO holders paid in October. And remember this is just a dating app.

We also know Blackstone used lead left underwriter Goldman Sachs‘ new-fangled hybrid auction process (also used on the DoorDash and Airbnb IPOs late last year) to try to get a better IPO price than it might from a traditional bookbuild. Yet the stock still ran, probably because the Bumble name was recognized and resonated with the Robinhood/retail crowd in the aftermarket.

And remember all this is happening during Covid-19, a time when the romantic notions have been thwarted by everyone being confined in their homes (though this WSJ article suggests use of dating apps during Covid rose strongly).

The bullish view on Bumble is that its operating model of only letting women make the first move will mean that many, many women will join its site and the men will have no choice but to follow.

And while Bumble is not nearly as profitable as its more diversified rival and comp, Match, Bumble has big earnings upside as it improves its margins to Match’s level. Bumble’s adjusted Ebitda margin was 26.3% in the period from January 29, 2020 to September 30, 2020, whereas Match margin is consistently up around 40% (the IPO filing is here, incidentally).

Maybe Bumble is a great investment and, yes, it is tough to be short at the moment.

But in a market many believe is priced for perfection, there are at least a few reasons to wonder whether Bumble can meet the lofty expectations now built into its stock price.

For one, ask yourself why Blackstone cashing in its investment so aggressively and so quickly.

Logically it would have been better to wait for Bumble to show better post-Covid numbers, unless it turns out the post-Covid world is tougher and the dating app market more competitive than expected.

Of course, Blackstone is just being smart in taking advantage of a white-hot IPO market to effectively cash its original investment and leave only house money at risk.

By the way, there is nothing stopping women from making the first move on other dating apps. And if blocking men from doing so is such a winning strategy for Bumble, how hard is it for some other dating app to do the same? I just pose the question.

Also lost in the fanfare is that Bumble’s average revenue per paying user fell slightly last year, in part as it tweaked its subscription pricing during the pandemic. As the prospectus points out, if Bumble can’t get more money out of each existing paying user, it will have to rely more on turning non-paying customers into payers. Bumble is yet to really prove it can do that since only 2.5m of its circa-40m users are paying for the privilege. The point is that Bumble’s metrics are not as pristine as the stock price action seems to imply.

Personally I think this is yet another stock that has raced well ahead of its true value (it now trades at more than 25x trailing revenue). I think few investors in their hearts (!) would contest this statement. And with markets at a point at which it is hard to think they could get any better, to me it seems a decent bet that Bumble will struggle to maintain its current levels ($75.46 on Friday) once the post-IPO honeymoon period is over.

Sorry I haven’t posted for a while. I promise to do better.

I’ll start with this. Almost exactly a year ago, I told investors to consider GM stock since it looked cheap.

Now I admit there have been better investments out there (including Tesla) and a lot has happened in a year, not least Covid-19 and a flood of liquidity into financial markets driving much speculative excess. But even old GM is starting to shine:

General Motors’ one-year chart. Source: Refinitiv.